Do you like bargain stocks? How does 84% off sound? That’s how much the streaming-TV company’s stock is year(NASDAQ: ROKU) are declining from their pandemic-induced peak in 2021. These stocks have barely changed since the second half of 2022. in fact, with most investors seemingly afraid to dive in without more evidence that a recovery is underway.

However, as the old saying goes, the time to be afraid is when others are greedy. The time to be greedy is when others are afraid.

That’s the long way of saying that the crowd is looking right past a great opportunity here.

The overwhelming concern is understandable. After all, the company is not profitable and is unlikely to become profitable in the near future. Investors can also clearly see how crowded and competitive the streaming business has become.

However, for interested buyers who can take the risk, Roku is still a compelling prospect at its reduced price.

But first of all.

If you’re not familiar with it, as noted, Roku is a streaming TV technology name. It manufactures the small boxes attached to your TV that allow you to watch TV shows and movies available through apps like Amazon prime minister Netflixand The Walt Disney CompanyDisney+ just to name a few; many TVs now come with this technology already built into them.

However, TVs and streaming receivers are not its main business. Over 85% of its revenue and all of its gross profits actually come from advertising and serving its streaming service intermediaries like the aforementioned Disney+ and Netflix; also runs its own ad-supported streaming channel. His devices are merely a means to that end.

Whatever the business model is, it works. ComScore data shows that Roku controls an industry-leading 37% of the connected TV ad market in the United States (excluding cable). Similarly, media market research team Parks Associates reports that Roku accounts for 43% of active media playback devices in the country, surpassing Amazon’s comparable FireTV technology. Roku hasn’t focused much on foreign markets yet, but where it has, it’s gotten respectable traction there as well.

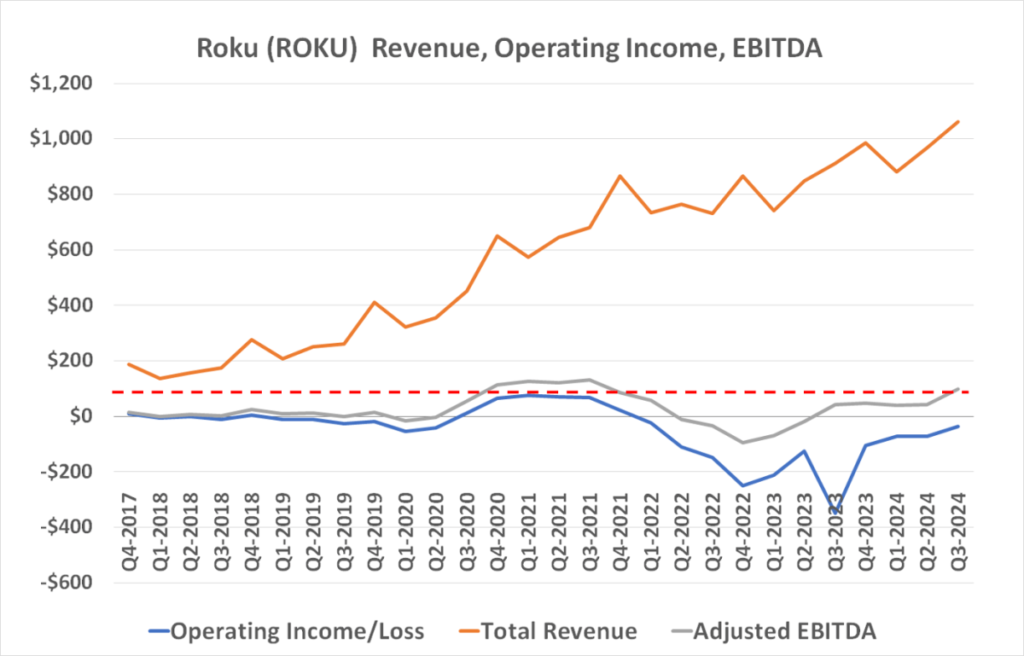

And the company is progress forward. Revenues continue to grow and losses continue to decrease.

Data source: Roku. Numbers are in the millions.

So why aren’t stocks behaving as if this progress is being made? Continue reading.

The Extreme Rise of Roku Stock in 2020 it makes obvious sense. Then the COVID-19 pandemic was in full swing, forcing millions of users to stay at home and do nothing but watch TV. And they did. In crowds. For perspective, ComScore says live TV viewing in the U.S. jumped about 70% year-over-year in March 2020.

Consumers have leaned heavily on Roku to facilitate this jump in TV viewing. Media device sales jumped 35% in the second quarter of 2020 alone, while the number of active Roku accounts improved 41% to 43.0 million over the same time period. This red-hot growth rate will not cool until the second half of 2021.

In retrospect, however, the 540% advance in Roku stock during that period was just too much. The Bear Market of 2022 finally forced a much-needed full correction on that massive gain. Indeed, the stock has barely budged since then, with many investors still reeling from the sheer scope of the setback.

However, this is one of those relatively rare cases where the disconnect that allows for a much-needed fix lingers too long. The parent company has proven that its financial viability is possible, even if it will take a few more years to get there; the analyst community is calling for a move to positive full-year earnings in 2026, when the company is expected to do business worth $5.3 billion.

Data source: StockAnalysis.com. Graphics by author.

The bulk of that business, of course, will still be ad revenue—the streaming portion of the overall ad business that eMarketer believes is set to grow at an average annual rate of 10% until 2027. Roku is positioned to enjoy more than its fair share of that growth, taking the company from the red to the black in that relatively short amount of time.

Investors haven’t yet said they’re willing to buy the stock as much as they did in 2020 before it falls in 2022. Analysts don’t fully agree either. Most of them only consider Roku stock a hold, while their consensus price target of $83.13 is only about 8% above the stock’s current price. That’s not much upside help.

However, neither the analyst community nor investors in general are always right about the likely near and far future of stocks. Sometimes you have to make a judgment call that most others don’t seem to agree with. This might be one of those times.

A guaranteed winner? Certainly not. There is above average risk combined with above average upside potential of this particular ticker. It is also far from a foundational type of holding for one’s portfolio.

However, there is less risk than the crowd seems to think there is, and that can be said more reward than most see. Sooner or later – and probably sooner than later — the market will have no choice but to reconnect these stocks with the underlying company’s continued growth. You’d be better off owning some Roku stock before that starts happening than being forced to chase it higher once the big move finally starts to unfold.

Have you ever felt like you missed the boat on buying the top performing stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issue a Double Down promotion. a recommendation for companies that they think are about to exit. If you are worried that you have already missed your chance to invest, now is the best time to buy before it is too late. And the numbers speak for themselves:

Nvidia:if you invested $1000 when we doubled in 2009,you will have $348,216!*

apple: if you invested $1000 when we doubled in 2008, you will have $47,425!*

Netflix: if you invested $1000 when we doubled in 2004, you will have $480,681!*

We’re currently issuing ‘double up’ signals for three amazing companies, and there may not be another chance like this anytime soon.

John Mackie, former CEO of Whole Foods Market, a subsidiary of Amazon, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions and recommends Amazon, Netflix, Roku and Walt Disney. The Motley Fool has a disclosure policy.